Home Insurance for Sarjapur Road Apartments: Structure & Contents Cover 2026

Published 13 Jul 2026 · Last updated 13 Jul 2026

Most apartment buyers on Sarjapur Road spend months comparing loan rates and floor plans, then overlook home insurance entirely. A gated community's master policy may protect the building's common areas, but it almost never covers your own flat's interiors, fittings, appliances or personal belongings — and those are the things that are actually lost or damaged in a fire, a burst pipe or a burglary. For an asset the size of a Sarjapur Road apartment, a home insurance policy is a small annual cost against a potentially large risk. This guide explains the two main types of cover, how to set the sum insured correctly, and what buying and claiming actually involves.

The frame of reference here is our featured pre-launch, Prestige Sarjapur Road by Prestige Group, with 1, 2 and 3 BHK homes from about ₹68.25 L at Ittangur. For the wider corridor, see our Sarjapur Road guide. Insurance policy terms, sums insured and claims procedures vary by insurer and are subject to IRDAI regulation; the points below are a general framework, not a quote or advice for any specific policy.

Why Apartment Owners Need Home Insurance

The building's structure — the columns, slabs, external walls — is typically built and sometimes insured by the developer or the resident welfare association. But everything inside your flat from the point of possession is your responsibility: the flooring, wall finishes, kitchen cabinets, bathroom fittings, electrical wiring inside the flat, air conditioners, refrigerators, televisions and everything you bring in. A fire starting in a neighbouring unit, a monsoon-season water ingress, a burst pipe or a break-in can damage or destroy any of these with no recovery path unless you have a policy.

Home insurance in India is not mandatory for apartment buyers — but lenders sometimes strongly encourage or bundle it with a home loan, and the cost relative to the sum at risk is low.

Structure vs Contents: What Each Covers

The two core types of cover address different things. Structure insurance (also called building or dwelling cover) applies to the physical shell of your flat — walls, floors, ceiling slab, doors, windows, fixed plumbing and embedded wiring. If a fire damages the walls and floors of your flat, structure cover pays to reinstate them. Contents insurance covers the movable items inside: furniture, kitchen appliances, electronics, clothing and declared valuables. Both can be bought as separate policies or combined in a single comprehensive home insurance plan.

| Cover type | What it protects | What it typically excludes |

|---|---|---|

| Structure / building | Walls, floors, ceiling, fixed plumbing, embedded wiring, fixed kitchen units | Movable items, land value, common areas (covered by RWA policy), gradual wear |

| Contents | Furniture, appliances, electronics, clothing, valuables (if declared) | Motor vehicles, business stock, items left outside the flat, undeclared high-value jewellery |

| Combined / comprehensive | Both of the above in one policy | Perils not listed; pre-existing damage; wilful acts |

How the Sum Insured Is Calculated

Getting the sum insured right is the most important decision in buying home insurance, because underinsurance means a partial payout at claim time. For structure cover, the sum insured should reflect the reinstatement cost — what it would cost to rebuild or repair your flat at current construction rates — not the market value of the property. In a rising market the property value includes the land and appreciation, which the insurer does not replace; they replace the physical structure. The reinstatement cost per square foot varies by finish quality and is usually well below the market price per square foot.

For contents, the approach is different: you make a list of items and their current replacement cost, and that total becomes the sum insured. Some policies use replacement value (new-for-old); others use depreciated (indemnity) value. New-for-old pays more at claim time but costs a slightly higher rate. Undervaluing contents is common — people forget air conditioners, kitchen appliances and all the small items that add up quickly.

| Item | Basis for sum insured | Common mistake |

|---|---|---|

| Structure / building | Reinstatement cost (rebuild at current rates), not market price | Insuring at property market value — massively overinsured on land; underinsured on structure |

| Contents | Replacement cost of all movable items, at today's prices | Forgetting appliances, kitchen items or undervaluing electronics |

| Valuables (jewellery, art) | Declared value or appraisal; stated separately in most policies | Assuming contents cover includes jewellery without declaring it |

Home-Loan Insurance vs Home Insurance

These are frequently confused but solve entirely different problems. Home-loan insurance — sometimes sold as mortgage reducing term assurance or home loan protection — is a life insurance product that pays off the outstanding loan balance if the primary borrower dies during the loan tenure, so the family is not left with the debt. The cover decreases as the loan is repaid. Home insurance, on the other hand, covers physical damage to the property itself. One protects the family from the liability; the other protects the asset from damage.

Lenders sometimes bundle a home-loan insurance product at disbursal — the cost is often added to the loan principal, which means you pay interest on it for the full tenure. Compare that cost against an independently bought term plan, which often provides more coverage more cheaply.

How to Choose a Policy

Look at three things first: the list of covered perils (does it include fire, flood, earthquake, theft and burst pipes at a minimum?), the claims settlement ratio of the insurer (publicly reported by IRDAI annually), and the exclusions — specifically whether gradual seepage, electrical breakdown, or wear-and-tear are excluded. Comprehensive single-policy cover that bundles structure and contents is simpler to manage than two separate policies from different insurers. Check whether the policy is on a reinstatement basis or an indemnity basis; reinstatement (new-for-old) is better at claim time.

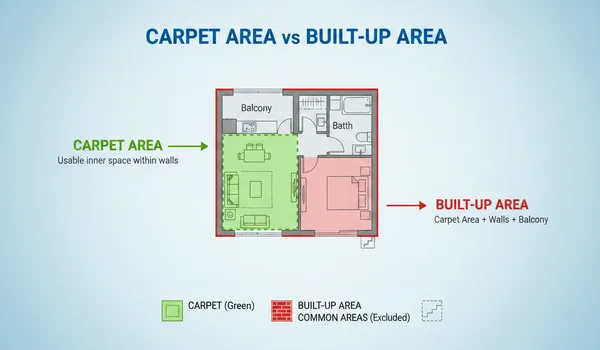

Verify the project's K-RERA completion and possession timeline before buying structure cover, since a policy on an under-construction flat may be structured differently and the insurable interest starts at possession. Activity across Bengaluru's Sarjapur Road corridor means the area is well-mapped by major insurers. Review the flat's built-up area and specifications on the floor plans before computing the sum insured, and check overall cost-of-ownership data on the price list. Contact the developer through the contact page for the handover schedule and finishing specifications, which inform the rebuild cost.

How Claims Work

In the event of damage, notify the insurer as soon as possible — most policies require prompt intimation, and delay can be used as a reason to dispute a claim. Document the damage thoroughly with photographs before any repair work begins; do not clear debris or carry out emergency repairs beyond what is needed to prevent further damage without first informing the insurer. The insurer will then depute a licensed surveyor to assess the loss and verify it against the policy schedule.

Keep your policy schedule, payment receipts and inventory list of contents in a safe place separate from the flat itself — if the flat is damaged, you still need those documents to file the claim. For an apartment in a gated community, also check whether the RWA's master policy covers any part of the event, as subrogation or coordination clauses may apply.

Frequently Asked Questions

1. Do I need home insurance for my apartment in Sarjapur Road?

It is not legally mandatory, but it protects what is often the largest asset you own. A gated community's master policy may cover the building shell, but it typically does not cover your flat's interiors, fixtures or belongings — so a separate policy is worth having.

2. What is the difference between structure and contents cover?

Structure cover insures the physical shell of your flat — walls, roof slab, floors and fixed fixtures like electrical wiring and plumbing. Contents cover insures movable items inside: furniture, appliances, electronics and valuables. Both can be bought separately or combined in one policy.

3. How is the sum insured for an apartment calculated?

For structure, the sum insured is typically the reinstatement cost — what it would cost to rebuild the flat at current construction rates, not the market price. For contents, you list the items and insure them at replacement or depreciated value depending on the policy type.

4. Is home-loan insurance the same as home insurance?

No. Home-loan insurance, or mortgage reducing term assurance, pays off the outstanding loan balance if the borrower dies during the loan tenure. Home insurance covers physical damage to the property and its contents. Both solve different risks and are usually bought separately.

5. Does a gated community master policy cover my flat?

The resident welfare association may hold a master policy covering the common areas and the building's external shell, but it rarely covers the interior of individual flats, including your flooring, kitchen fittings, electronics or personal belongings. Check the RWA policy schedule before assuming you are covered.

6. What events are usually covered by a home insurance policy?

Standard perils typically include fire, lightning, explosion, storm, flood, earthquake, burst pipes, theft and accidental damage, depending on the policy. Exclusions often include gradual wear and tear, wilful damage, pre-existing damage and certain valuables unless specifically declared.

Conclusion

Home insurance is the protection most Sarjapur Road apartment buyers arrange last, if at all — yet it covers the interiors and contents that a community master policy does not, at an annual cost that is small against the value at risk. The two distinct types are structure cover, which insures the physical flat at reinstatement cost, and contents cover, which insures your movable belongings at replacement value. Setting the sum insured correctly is more important than any other decision: insure the structure at rebuild cost, list all contents at today's replacement price, and declare valuables separately. Home-loan insurance is a different product that clears the loan if the borrower dies, not a substitute for property cover. Compare perils, claims settlement ratios and indemnity vs reinstatement basis before you buy, and notify your insurer immediately if damage occurs. Check Prestige Sarjapur Road's floor plans for built-up area, review the price list for cost context, and contact the developer for finishing specifications that set the rebuild cost before you compute the sum insured.

Prestige Sarjapur Road Blog